Market Volatility Resets Leadership—and Creates Opportunity

April 2025

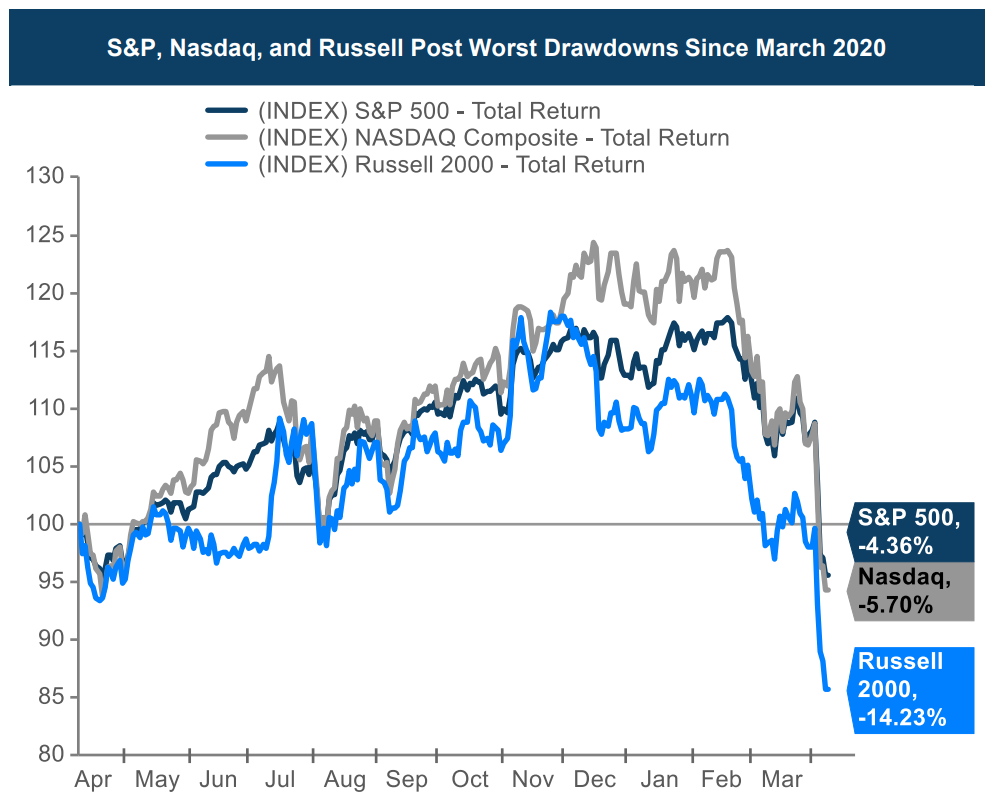

The first quarter of 2025 delivered a sharp reminder that market leadership is rarely permanent. What began as a continuation of 2024’s momentum—new highs, narrow leadership, and confidence in a soft landing—ended abruptly in March as trade policy shocks, weakening data, and rising recession fears triggered a swift and broad market correction

Triggered by the announcement of an aggressive “Liberation Day” reciprocal tariff regime, the selloff was both sudden and severe. All major U.S. equity indices fell sharply, culminating in the worst two-day decline for the S&P 500 since March 2020. By quarter-end, nearly half of U.S. equities were down more than 35% from their 52-week highs, underscoring how rapidly risk was repriced across the investable universe.

Source: FactSet as of4/9/2025

The End of Easy Leadership

One of the most notable developments of the quarter was the unwind in prior market leaders. The “Magnificent Seven,” which had dominated returns over the past two years, became a source of funds as investors reassessed both valuation and growth durability. Several mega-cap technology stocks experienced double-digit declines, with drawdowns rivaling or exceeding those of the broader market

This shift reflects more than simple profit-taking. Cracks have emerged in the AI-driven growth narrative, particularly following January’s DeepSeek-related volatility. Concerns around the sustainability of AI capital expenditures, moderating cloud spend, and diminishing incremental earnings upside have prompted investors to rotate toward balance sheet strength, cash flow durability, and defensive growth. Notably, the equal-weighted S&P 500 outperformed its cap-weighted counterpart during the quarter—a clear signal that leadership has broadened and become more selective.

Tariffs, Policy Uncertainty, and Recession Risk

Trade policy uncertainty loomed over markets throughout the quarter but ultimately proved far more disruptive than anticipated. According to Goldman Sachs, the effective U.S. tariff rate is poised to rise by approximately 20%, exceeding even levels seen during the Smoot-Hawley era and effectively erasing decades of trade liberalization

The implications are significant. Higher tariffs introduce new inflationary pressures, weigh on global growth, and materially increase recession risk. Retaliatory actions—most notably China’s 34% tariff on U.S. goods—have heightened concerns about a prolonged global trade conflict. Equity markets responded accordingly, with volatility spiking to levels not seen since the early days of the pandemic and U.S. equities underperforming the rest of the world by the widest margin since 1988

Valuations Reset, but Risks Remain

Despite the sharp selloff, valuations remain elevated relative to prior market troughs. The S&P 500 continues to trade near 18x forward earnings—well above levels reached during recent periods of stress in 2018, 2020, and 2022. With tariffs introducing meaningful downside risk to both earnings and GDP forecasts, further multiple compression remains a possibility, particularly in growth-oriented segments of the market

At the same time, sentiment indicators suggest markets have moved into oversold territory. Extreme downside moves of this magnitude have historically been rare, and past episodes of similar volatility have often been followed by strong forward returns over the subsequent 12 months. While history does not repeat perfectly, it does highlight that periods of indiscriminate selling often lay the groundwork for opportunity.

Source: Goldman Sachs GiR, as of 4/2/2015

Finding Opportunity Amid the Volatility

In this environment, differentiation matters. Tariff exposure is emerging as a key driver of relative performance, creating clear winners and losers across sectors. Areas with domestic supply chains, pricing power, and policy insulation—including health care, select biotechnology, utilities, and parts of the U.S. housing ecosystem—have demonstrated relative resilience. By contrast, consumer discretionary, autos, hardware, and Asia-exposed multinationals face greater margin and earnings pressure

Within health care, biotechnology stands out as a compelling example of mispriced opportunity. The sector benefits from tariff insulation, strategic policy support, and renewed M&A interest as large pharmaceutical companies seek to replenish pipelines amid attractive valuations. Despite these tailwinds, biotech has been treated as high-beta risk rather than defensive growth—creating a fertile environment for active stock selection focused on strong pipelines and balance sheet quality

Looking Ahead

We expect markets to remain volatile in the near term, with a “sell-the-bounce” mentality likely to persist until greater clarity emerges around tariffs, economic growth, and monetary policy. A durable market bottom may not materialize until later in 2025, once recession risks peak or policy conditions improve.

In the meantime, our focus remains on capital preservation, disciplined valuation, and selectively upgrading portfolio quality. Periods of stress often provide the opportunity to build positions in long-term compounders at attractive margins of safety. While uncertainty remains elevated, volatility can be an ally for patient investors willing to look beyond the headlines.