Market Views – 3Q 2024

Broadening Participation Amid Shifting Leadership

Despite intermittent volatility during the third quarter, U.S. equity markets continued to climb, with major indices reaching fresh all‑time highs. A fading recession narrative, easing inflation pressures, and an important shift in Federal Reserve policy combined to support risk assets. At the same time, market leadership broadened meaningfully, marking a notable change from the narrow, mega‑cap‑driven environment that defined the first half of the year.

A Strong Start, Supported by Policy Tailwinds

The S&P 500 posted its best start to a year since the late 1990s, underscoring investor confidence even as economic data remained mixed. Cooling inflation and softening labor market indicators gave the Federal Reserve the flexibility to begin easing monetary policy, culminating in its first rate cut in September. This shift provided relief to interest‑rate‑sensitive areas of the economy and reinforced expectations for additional cuts over the coming years.

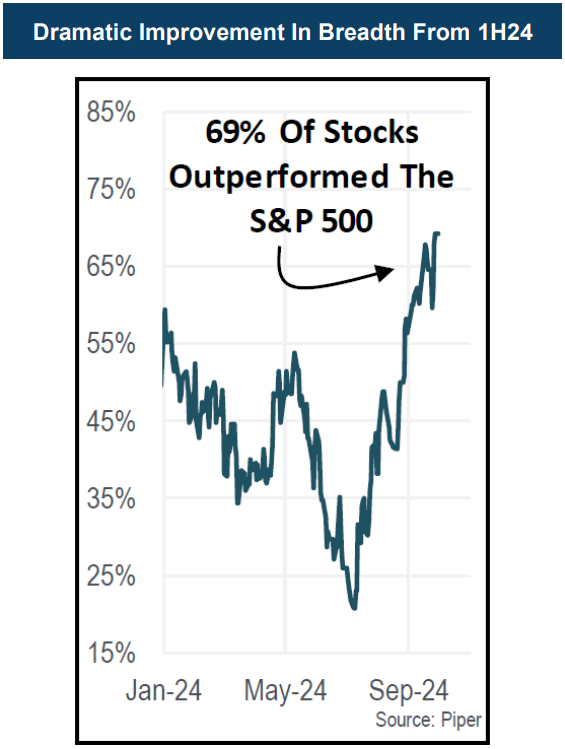

Market Breadth Improves as Leadership Rotates

One of the most important developments of the quarter was the dramatic improvement in market breadth. After an extremely narrow first half dominated by a handful of mega‑cap growth stocks, participation widened as other sectors and styles began to catch up. Large Growth, which led earlier in the year, reversed sharply and lagged as rate‑sensitive and defensive areas rallied.

The so‑called “Magnificent Seven” illustrated this shift clearly. After peaking in relative performance in July, the group underperformed the broader market through the remainder of the quarter, reflecting a healthier and more balanced market environment.

Source: Piper Sandler, as of 10/1/2024

Quality Remains in Favor

While leadership rotated across size, style, and sector lines, factor performance remained remarkably consistent. High‑quality companies, along with momentum and size factors, continued to outperform year‑to‑date. In contrast, volatility‑heavy and lower‑quality segments lagged, even after a brief speculative rally in July sparked by optimism around Fed easing.

This persistence highlights investors’ ongoing preference for durable balance sheets and reliable earnings in an evolving macro environment.

Fed Policy Shifts, but Labor Signals Bear Watching

With inflation trending lower, the Federal Reserve’s attention has shifted squarely to the labor market to guide the pace of future rate cuts. While headline employment data has remained resilient, leading indicators such as hiring and quits rates suggest caution may be warranted. A stronger‑than‑expected September jobs report raised questions about how quickly policy will normalize from here, reinforcing expectations for a measured and data‑dependent path forward.

Valuations, Earnings, and the Case for Selectivity

Valuations across the market are increasingly mixed. Large‑cap equities trade near cycle‑high multiples, while small‑caps sit near historic relative troughs. Although small‑cap earnings expectations have deteriorated, history suggests that periods like this often precede meaningful relative recoveries—albeit with patience required.

At the same time, earnings growth drivers are broadening beyond the largest technology companies. Improving expectations for the broader market relative to the Magnificent Seven support the case for continued diversification and active security selection.

Source: Furey Research Partners, Factset, as of 9/30/2024

Outlook: Opportunity Amid Uncertainty

Looking ahead, markets are balancing constructive fundamentals against elevated uncertainty. Inflation continues to moderate, credit conditions remain benign, and policy easing is occurring against a stable economic backdrop. However, elevated valuations, geopolitical risks, and election‑related volatility are likely to keep markets choppy.

We believe the recent broadening in market participation is a healthy development and that select opportunities remain attractive—particularly in areas where valuations and expectations are more subdued. As always, patience and discipline remain essential as the market navigates the final stretch of the year.