Market Momentum Masks Growing Concentration Risks

January 2025

U.S. equity markets delivered another exceptional year in 2024, powered by resilient economic growth, easing inflation, and an ongoing surge in enthusiasm around artificial intelligence. The S&P 500 posted more than 20% returns for a second consecutive year — a rarity last seen during the late-1990s technology boom — while recording 57 new all-time highs along the way. Yet beneath these headline results, market leadership grew increasingly narrow, setting the stage for a more complex and potentially volatile environment in 2025.

A Record Year — With Familiar Drivers

Economic momentum consistently exceeded expectations in 2024. Job creation remained robust, consumer spending proved resilient, and both earnings and GDP growth surprised to the upside. Inflation continued its gradual descent, allowing the Federal Reserve to initiate its first rate cut since 2019 in September. Equity markets responded favorably, with U.S. stocks once again dominating global performance.

However, the gains were far from evenly distributed. Large-cap growth stocks led markets for a second straight year, marking the strongest two-year growth versus value outperformance on record. Small-cap equities lagged yet again, extending a streak of underperformance versus large caps that now stretches back to 2017.

Leadership Narrowed Further

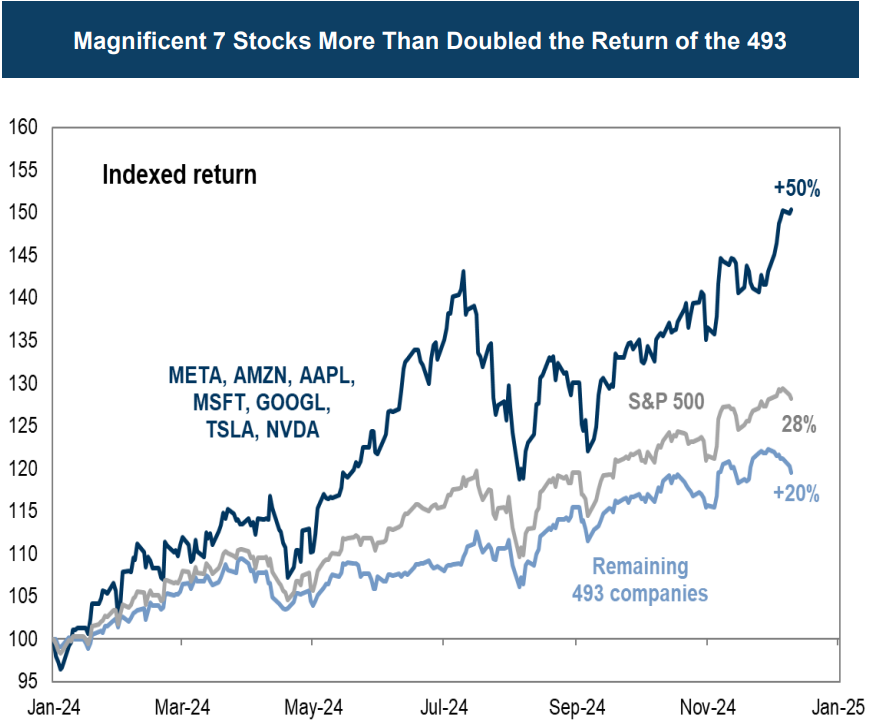

Market concentration intensified meaningfully. The so-called “Magnificent 7” stocks once again accounted for a disproportionate share of index returns and now represent more than one-third of the S&P 500’s total market capitalization. Sector leadership also remained unchanged from 2023, with Communication Services, Technology, and Consumer Discretionary repeating as top performers and besting the weakest sectors by more than 30 percentage points.

Momentum emerged as the dominant investment factor for much of the year, significantly outperforming value, quality, and low volatility. While a modest rotation into cyclicals and value appeared late in the fourth quarter, high-beta and highly speculative areas surged into year-end — a dynamic that historically has proven difficult to sustain.

Source: Goldman Sachs Global Investment Research, Scott Rubner, as of 12/12/2024

Policy Shifts and Post-Election Optimism

Political developments also played a role in late-year performance. Markets rallied sharply following the U.S. election, driven by expectations for deregulation, tax cuts, and pro-business policies. Cyclicals, financials, and crypto-related assets were among the biggest beneficiaries, while investor sentiment surged alongside record inflows into U.S. equities.

At the same time, policy uncertainty remains elevated. While the Fed has pivoted toward a more accommodative stance, inflation remains sticky, and Westfield does not expect additional rate cuts in 2025. Markets, however, continue to discount a more aggressive easing cycle — a disconnect that could challenge valuations if inflation reaccelerates or growth cools.

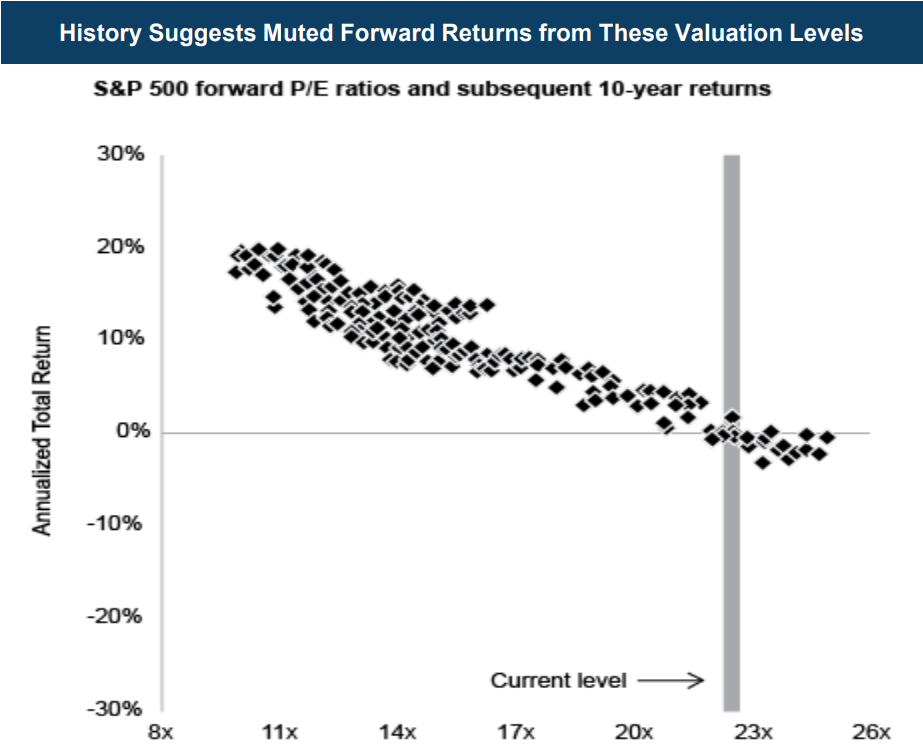

Valuations and Sentiment Leave Little Margin for Error

Several cautionary signals warrant close attention. Valuations, particularly within large-cap growth stocks, remain elevated relative to history. Retail speculation has increased sharply, with leveraged long ETF assets vastly outweighing short exposure. Housing and used-car markets are showing signs of strain, raising questions about the durability of consumer spending should financial conditions tighten.

At the same time, not all areas of the market appear equally stretched. Select cyclicals, small caps, and value-oriented segments trade at more compelling relative valuations, and structural tailwinds — including AI investment, reshoring, and infrastructure spending — continue to support longer-term growth.

Source: Oaktree Capital Management, as of 1/7/2025

2025 Outlook: Balance Is Warranted

Looking ahead, the investment backdrop calls for moderation rather than complacency. Interest rates may remain higher for longer, policy missteps remain a risk, and market leadership appears ripe for rotation. While growth and technology retain long-term structural appeal, opportunities are likely to broaden across cyclicals, health care, materials, and GARP-oriented strategies as 2025 unfolds.

After two years of exceptional returns driven by a narrow group of winners, investors may need to recalibrate expectations. A more balanced approach — emphasizing diversification, valuation discipline, and flexibility — appears increasingly prudent in the year ahead.