The Current Environment

The software sector is facing its most fundamental repricing in over two decades. Unlike prior corrections – 2000, 2008, 2011, 2016, 2018, and 2022—where concerns centered on cyclical deceleration or valuation normalization, today’s fear is structural obsolescence: the belief that AI enables replacement of existing software incumbents. The market isn’t asking “how much slower will they grow?”—it’s asking “will they exist?”

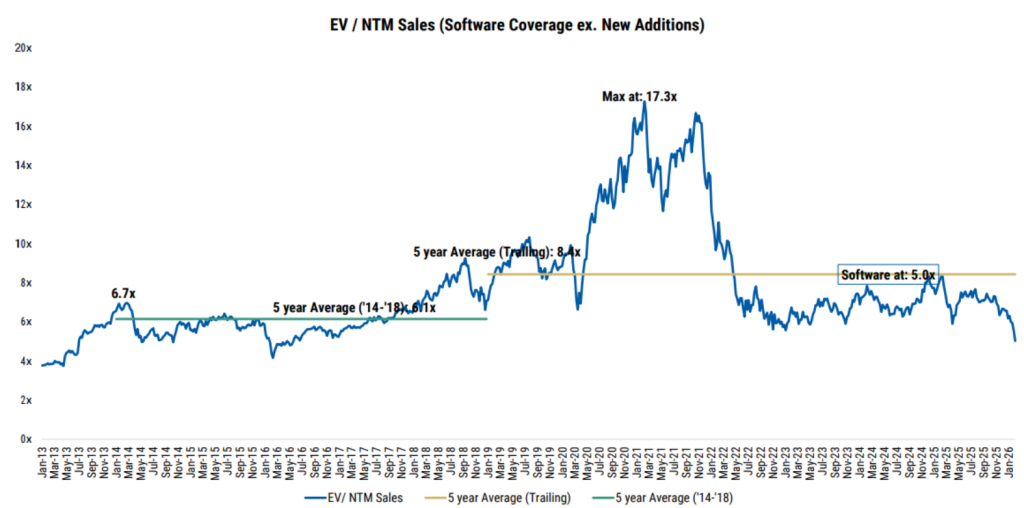

Valuations have compressed to levels not seen since the Covid lows in 2020, with the median software company now trading 50-60% below its five-year average. Current prices suggest the market is embedding extreme contraction for platform leaders implying substantial customer attrition and revenue declines. These aren’t conservative estimates: they’re depression-level scenarios. The narrative shifts with extraordinary speed—a single post from a leading AI lab can reprice the entire sector by 10% in a session. Execution doesn’t necessarily matter either. Quality companies reporting strong quarters are still trading down over 25%. When platforms generating 30%+ free cash flow margins trade at distressed valuations last seen during the global financial crisis, in our view, the market is pricing for terminal decline, not temporary disruption.

Software valuations have compressed dramatically, trading ~50% below the 5-year average.

Source: Morgan Stanley Research, FactSet, Company data, as of 2/9/2026

Even software stocks insulated from the AI displacement threat have been hit hard

Note: Blue line is software that AI cannot realistically displace because they require physical execution, regulatory entrenchment, integration complexity, or human accountability, and businesses that benefit directly from increased AI usage – compute, data infra, observability, security, hyperscale cloud, AI development platforms (GSTMTSOL); Black line is all US software; Red line is software-tilted workflows that AI could increasingly automate or rebuild internally, potentially reducing need for outsourcing (GSTMTSOS)

Source: Goldman Sachs FICC & Equities, Bloomberg, as of 4/10/2026

This Environment Demands Differentiation.

Over the past month we have conducted an intensive series of conversations with enterprise CTOs, system integrators, resellers, and cloud providers to calibrate what is actually happening in production environments today versus what is being debated online. When an entire sector reprices on existential concerns, the temptation is to buy the basket. But some companies will survive and thrive through this period. Others genuinely face displacement. Fundamental research and active management are essential to separate survivors from the disrupted.

The AI Disruption Debate

Four legitimate disruption vectors exist:

- AI overviews negatively impact lead generation for small and medium sized businesses (SMB)

- Productivity gains reduce seat needs

- “Vibe coding” threatens simple products, especially in SMB

- Agents transition from augmentation to replacement

These concerns are real. AI’s advancement has consistently surprised even bullish observers.

However, the market is conflating “AI can write code” with “enterprises will replace mission-critical systems.” Through comprehensive primary research with enterprise CIOs and IT organizations, we hear a consistent message: customers want vendors to bring AI to them: embedded in products, using their data, not forcing them to build it themselves. LLMs by themselves generate probabilistic outputs, which are useful for content creation and general queries, but enterprise operations require deterministic answers: which invoice to pay, which approval path to trigger, which compliance rule applies. Achieving this requires business context from systems of record, not generic inference—which is precisely why CIOs expect to keep the platforms they already use and pay the same or more for AI functionality that improves the product. No CIO says “we’re having Claude write us a CRM replacement.” The gap between consumer AI demos and enterprise production requirements remains substantial.

Enterprise platforms operate business processes as a service, managing reliability, security, compliance, and governance at scale. Open-source alternatives have existed for over a decade, yet incumbents haven’t been replaced. Generating code is not the same as operating a mission-critical business process at enterprise scale. History reinforces this: when cloud threatened perpetual license models in the 2010s, the market feared software companies would lose pricing power and destroy value. Instead, the industry successfully transitioned to subscriptions, often at higher lifetime values. Seat-based pricing will similarly evolve, likely toward consumption or outcome-based models, but the underlying value equation persists: enterprises pay for reliability, security, and operational complexity at scale.

That said, we cannot easily disprove the disruption thesis. It must be proven over multiple quarters.

The scenario we watch most carefully is one in which AI becomes a true abstraction layer above enterprise applications. In this architecture, autonomous agents function as the workers, communicating and executing at a level above specific software platforms and interacting with underlying applications and data only through APIs. If this model achieves broad adoption in production, the implications for software revenue models are profound. Per-seat pricing would give way to consumption or token-based pricing tied to agent activity, potentially at rates set as a fraction of the human labor cost being displaced. The race to define this interface is intensifying: incumbent systems of record are building their own agents to retain the customer relationship, while generic AI platforms attempt to become the universal orchestration layer. Which model prevails—workers entering vertical applications with embedded agents, or workers issuing commands to a generic AI that never surfaces the underlying application—remains an open and critical question. We have not yet observed this abstraction model operating at scale in a true enterprise production environment, but we monitor for it daily.

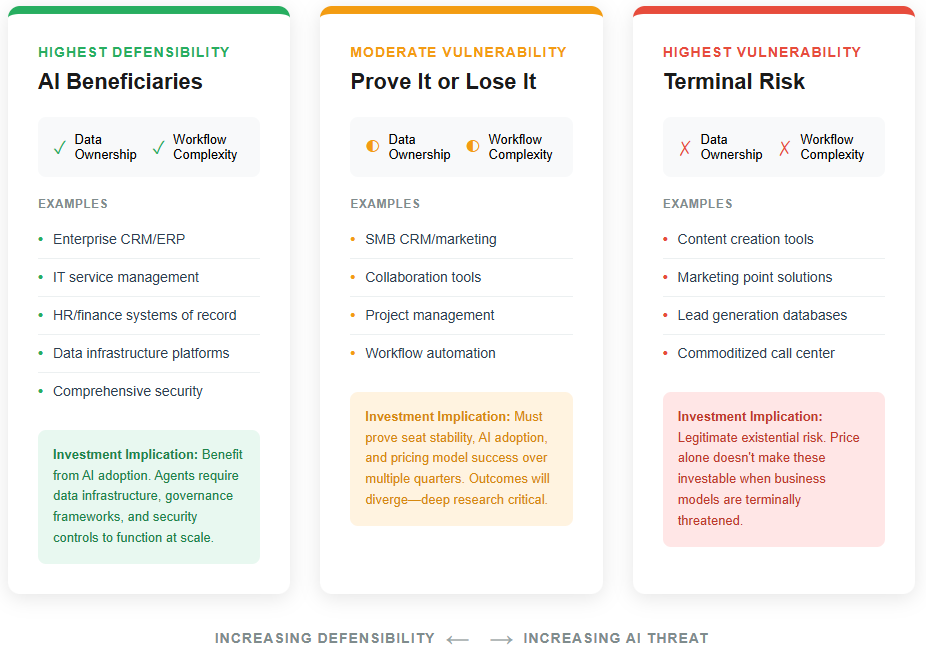

The Vulnerability Spectrum

Not all software companies are equally positioned. Two characteristics matter: Data Ownership (proprietary, business-critical data) and Workflow Complexity (millions of customized workflows built over decades). Companies possessing both moats benefit from massive switching costs and multi-year implementation investments that won’t be abandoned. Companies lacking both are genuinely vulnerable.

Current Evaluation Framework

We acknowledge this framework is dynamic and will evolve as the data evolves. We are being intellectually honest about what we know, what we observe, and where genuine uncertainty remains.

More constructive:

- Enterprise systems of record possessing both proprietary data accumulated over decades and complex workflows built through multi-year, multi-million dollar implementations.

- Incumbent software vendors using AI code generation to strengthen rather than compete against their existing workflow complexity.

- Security platforms where AI adoption creates exponentially more threat data and requires increasingly sophisticated response workflows.

- Data infrastructure companies that reinforce rather than undermine data ownership by controlling access pathways between AI systems and business-critical information.

More cautious:

- Software serving small and medium businesses, which typically lacks both proprietary data and complex workflows while facing customers with lower switching costs and greater willingness to experiment with AI-generated alternatives. The exception is companies with deep vertical expertise that creates genuine data ownership and workflow complexity difficult to replicate with generic AI solutions.

Conclusion: Selectivity, Patience and Active Management

This framework-driven analysis reveals that the software sector will experience unprecedented dispersion in outcomes. The market currently treats all software companies as facing similar disruption risks, creating opportunity for those willing to distinguish between defensive and vulnerable business models.

This creates opportunity for patient capital: when companies demonstrate sustained resilience through seat stability, ramping AI revenue, and successful pricing transitions, we believe they will be rewarded disproportionately as the market re-rates from the perception of terminal-value decline to durable growth. For disciplined investors willing to separate survivors from the disrupted, now may represent a durable entry point for quality franchises trading at irrational prices.

Important Disclosures

The views expressed are those of Westfield Capital Management Company, L.P. as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable.

Past performance is not indicative of future results.